The first three columns are the same as the single column cashbook and show the date, transaction description (Desc.), and ledger folio reference (LF). The two columns referred to in the name of this cashbook are the monetary amount of the cash remote tax preparer jobs, work from home online receipt (Cash), and the monetary amount of the discount allowed (Discount) both highlighted in gray. A cash book with three columns for discounts received and paid, cash transactions, and bank transactions is known as a three column cash book.

Advantages of Double Column Cash Book

We will explore various types of cash books, such as single-column, double-column, single-entry, and double entry. Additionally, we will discuss the benefits of using an accounting package for your cash book management and introduce our Free cash book template. When David deposits money with the bank, he makes an entry on the debit side of his cash book.

What is a three column cash book?

A petty cash book also refers to the book in which small payments are recorded, which are not convenient to record in the main cash book. For a manufacturing company with stable earnings and a predictable return on equity, residual income valuation can provide a straightforward measure of economic profit. This approach is particularly useful for mature companies with reliable net income but limited growth prospects. Banks and financial institutions are often challenging to value using traditional cash flow models due to complex capital structures and regulatory requirements. Instead, residual income valuation can be effective because it focuses on accounting-based metrics like book value and net income. By subtracting the required return on equity from net income, analysts can estimate the bank’s economic profit and gain a better understanding of whether it’s generating value over its capital cost.

Question 3

The right hand, payments side (credit) would be identical in structure and format. The cash book is a chronological record of the receipts and payments transactions for a business. An overview of this procedure is given on the double column cash book page. The second type of cash book is called the double-column cash book. As the name implies, there are two columns for this type of cash book. It allows users to keep more detailed notes about their transactions.

It engaged in the following cash transactions during the month of September 2016. Cash books are important because they allow businesses to track their finances in a detailed and organized way. This information can be used to make important decisions about the future of the business. These will provide a detailed overview of the business’ financial health. A triple-column cash book (also known as a three-column) includes cash, bank and an additional column for discounts.

- The single-column cash book has only one money column, which is totaled and balanced like a traditional T-account.

- Let us understand the format of maintaining a petty cash book or a detailed cash book through the detailed explanation below.

- Prepare a double column cash book using the following transactions, and post the entries, therefore, to ledger accounts.

- By focusing on book value and earnings, the model helps analysts assess whether the utility’s investments are generating returns above the required rate, even in the face of heavy capital spending.

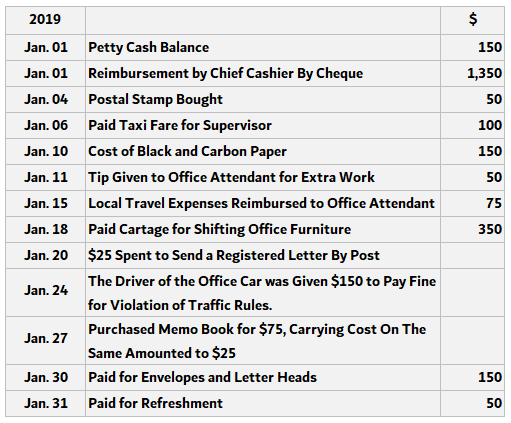

The position of the petty cash book is similar to a subsidiary book. The petty cashier is always assumed to hold cash equal to the imprest account in the form of actual cash or paid-up PCVs. When a petty cashier needs money, the main cashier gives them a cheque.

As this explanation indicates, the cash book is among the most important books of accounts in modern business. It should be noted that the amount spent by the petty cashier cannot exceed the amount received. In this case, cash is a lose term covering not only papermoney and coins but also cheques/checks, direct credits, electronic transferpayments, and so on. When reconciling the cash book to the bank statement you can select different red letters from a drop-down list. The following example summarizes the whole explanation of the triple-column cash book given above.

On the bank’s side, the record is usually kept in the form of a personal account. It is maintained more or less along the same lines as a businessperson maintains their personal accounts for debtors and creditors. When a payment is made, an original receipt is obtained from the payee. This receipt is called a credit voucher because it supports entries on the credit side of the cash book. This form of a cash book has only one amount column on each of the debit and credit sides of the cash book.